{kind=link}

New York Community Bancorp Inc. “is on its to own” to figure out its accounting and other issues as it faces fresh losses in its stock price and prepares to update its financials in the coming weeks.

That’s according to Citigroup analyst Keith Horowitz, who commented after the regional bank

NYCB,

disclosed “material weaknesses” in its accounting and other financial-reporting issues — news that sent its stock down 24% at midday Friday.

“We expect more questions on whether NYCB will sell, but we do not see a lot of potential buyers here even at this price due to the uncertainty,” Horowitz wrote in a note to clients.

While the material weakness “adds more fuel” to the fire around the bank, no additional financial impact is expected beyond the $2.4 billion goodwill impairment charge that it took for its fourth quarter, Horowitz said.

New York Community Bancorp’s stock fell to $3.66 a share in recent trades after the bank said late Thursday it found material weakness related to its loan review in an evaluation of its internal financial controls. The stock last traded at its current level in the late 1990s.

On Friday, the bank named George F. Buchanan III as vice president and chief risk officer, a position that had been vacant prior to the bank’s troubles this year. Buchanan comes to the bank with more than 30 years of experience including at First Union, which is now part of Wells Fargo & Co.

WFC,

and at AmSouth Bancorporation, US Bank and Regions Bank.

The bank also said it has named Colleen McCullum as its chief audit executive. McCullum has roughly 20 years of experience in the business.

Late Thursday, the bank said its internal-control deficiencies were the result of “ineffective oversight, risk-assessment and monitoring activities.”

A spokesperson for the Federal Deposit Insurance Corp. declined to comment.

Wall Street analysts were quick to point out that the troubles appear to be isolated around New York Community Bancorp, which is the holding company for Flagstar Bank.

J.P. Morgan analyst Steven Alexopoulos said the bank’s situation is “not representative of pressure/uncertainty on regional banks more broadly.”

Despite these assurances, shares of regional banks fell in early trading on Friday.

Citigroup analyst Horowitz said “significant changes” will be needed for New York Community Bancorp’s credit-risk monitoring, “which we expect may lead to them being more proactive on recognizing issues going forward.”

The bank’s disclosure that it does not anticipate a materially different operations disclosure is important, Horowitz said.

“A material weakness does not necessarily always equate to an impact on financials,” Horowitz said. “In our view, the delay in the 10-K is likely meant to give auditors sufficient time to ensure that there was no financial impact from the material weakness in the control environment, which means a lot of time for individual loan testing.”

Wedbush analyst David Chiaverini reiterated an underperform rating — the equivalent of sell — on New York Community Bancorp and cut his price target for the stock to $3.50 from $5.

“Our underperform rating is based on NYCB’s high exposure to [New York City] rent-regulated multifamily loans, which we believe are under stress, and represent 25% of NYCB’s total loans, which is the highest in our

coverage,” Chiaverini said.

J.P. Morgan’s Alexopoulos said the bank continues to pose risks and that investors should remain on the sidelines.

“While it doesn’t appear that the incidence of weakness in controls being identified would pose limitations on the company’s business/lending activities or result in a material increase in costs beyond what has been already identified along with [fourth-quarter 2023] results, this new information further elevates the uncertainty surrounding the company,” Alexopoulos said.

Piper Sandler analyst Mark Fitzgibbon downgraded New York Community Bancorp to neutral from overweight, saying that “the whack-a-mole at New York Community continues.”

The bank’s latest disclosure raises concerns “that there could be more issues coming down the pike for the company,” Fitzgibbon said.

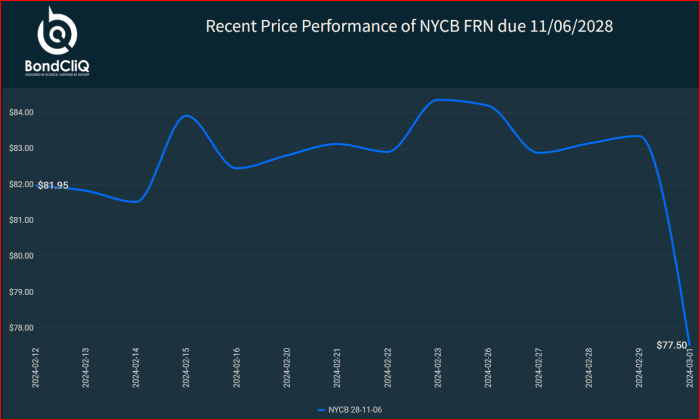

New York Community Bancorp’s sole bond offering — a $300 million bond it issued in 2018 — also traded sharply lower.

NYCB’s bond price is down sharply after the company’s material-weakness disclosure.

BondCliQ Media Services

New York Community Bancorp said it had appointed Alessandro DiNello as its new president and chief executive effective immediately, after Thomas Cangemi resigned from the roles after 27 years at the company. DiNello, the former chief executive of Flagstar, was appointed as the bank’s executive chair earlier this month, having previously served as nonexecutive chair of its board. Cangemi will remain on the board.

The developments marked the latest turn in a roller-coaster ride for the bank since it acquired the distressed Signature Bank, a former S&P 500 component, in a deal brokered by the FDIC following the collapse of Silicon Valley Bank one year ago.

Last summer, the bank reported a roughly 150% increase in second-quarter profit, which sent its stock higher.

Then the stock lost a third of its value on Jan. 31, in the largest one-day slide in its history, when the bank reported a surprise-fourth-quarter loss, a dividend cut and costs tied to two loans, one on an office property and the other a multifamily-property deal.

That triggered selling in other regional banks in early February as New York Community Bancorp’s stock price fell to levels not seen since the 1990s. Insiders then acquired stock at discounted prices, and the stock had been fighting its way back for the past couple of weeks. Among the buyers was billionaire George Soros, who bought about 1 million shares.

New York Community Bancorp boosted its loan-loss reserves by 790%, or $490 million, in the fourth quarter from the previous quarter, more than any other bank in its class, as it faced potential challenges in its office and multifamily-loan portfolio.

When the bank bulked up by buying Signature Bank, it reached a size that triggered higher capital requirements by regulators. This led the bank to set aside more money for its balance sheet.

The bank may have to take further steps to protect against bad loans, said Tomasz Piskorski, finance professor at Columbia University.

“NYCB has also some unique commercial real estate risks tied to their exposure to rent-stabilized multifamily financing that experienced significant price drops also due to recent rent regulation,” Piskorski said in an email to MarketWatch.

The FDIC may require the bank to increase its loss provisions.

“It’s plausible they are exploring options to raise additional capital or seek a strategic investor,” Piskorski said. “If these avenues prove unsuccessful and their challenges persist, leading to further deterioration of their capital position, the FDIC may step in for an outright takeover, or they may face a distressed acquisition by another bank.”

Brian Mulberry, client portfolio manager at Zacks Investment Management, said the bank’s executive team wasn’t fully prepared to absorb a business the size of Signature Bank.

While New York Community Bancorp’s new chief executive may manage to address the bank’s problems, “things are not going well,” Mulberry said.

For now, Mulberry agrees with other analysts that the trouble appears to be an isolated case at New York Community Bancorp, he said.

With bullish economic data likely to keep interest rates higher for longer this year, banks may face lower demand for loans, particularly in parts of the country with higher office space vacancies such as San Francisco and Seattle, he said.

Also read: New York Community Bancorp’s stock crushed on surprise loss, dividend cut and cost of two loans

Philip Van Doorn and Bill Peters contributed.